As a seasoned researcher with years of experience navigating the ever-evolving financial landscape, I find the recent report from the Financial Conduct Authority (FCA) regarding the high rejection rate of crypto registration applications both intriguing and concerning. The sheer number of rejected applications points to a significant challenge in maintaining effective anti-money laundering controls within the industry.

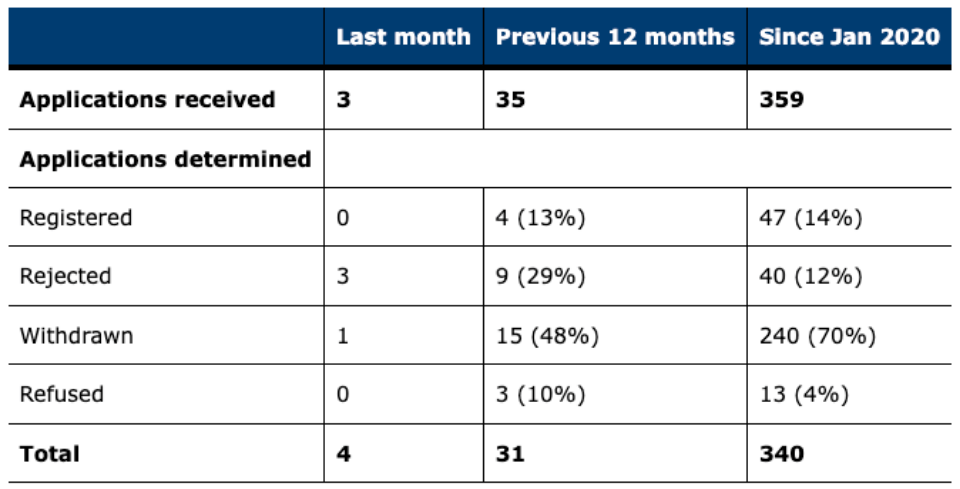

In the chaotic British environment surrounding cryptocurrencies, it was revealed by the Financial Conduct Authority that approximately 87 out of every 100 applications for crypto registration were unsuccessful during the previous fiscal year.

This is a staggering fact that brings up very serious questions concerning the effectiveness of anti-money laundering controls in the industry. Only four out of 35 applications were approved, underlining how tough the regulatory environment remains.

Struggling To Meet Standards

Since January 2020, the Financial Conduct Authority (FCA) has taken on the role of overseeing crypto-related businesses, ensuring they adhere to regulations related to money laundering, terrorist financing, and the transfer of funds.

In summary, the report indicates that a large proportion of companies do not meet the expected standards. This is primarily due to the fact that many applications were denied based on inadequate anti-fraud and Anti-Money Laundering (AML) measures, which are crucial for preventing illegal funds from entering the financial system.

FCA Chair Charles Randell commented:

“Although some firms have shown adequate systems, too many have failed to meet acceptable standards of risk management and controls to date, leading to this wave of rejections and withdrawals.”

As a researcher delving into the intricacies of financial regulations, I must admit that the introduction of the European Union’s MiCA framework, alongside other EU regulations, has undeniably added an extra layer of complexity to the landscape. Although these rules are intended to enhance the regulation of crypto assets, they also present a challenge for UK firms who are already grappling with local compliance matters, making their tasks even more daunting.

As the rules governing cryptocurrency operations in the UK are still under development, there is growing curiosity about whether this market will continue to be an attractive option for crypto-related activities.

Why the FCA rejected almost 90% of crypto firms’ applications

— DL News (@DLNewsInfo) September 5, 2024

A New Era Of Regulation

The FCA’s report supports a broader effort to strengthen oversight in the cryptocurrency market. This includes establishing a specialized “Crypto Unit” within the National Crime Agency, granting it greater power to tackle criminal activities linked to digital currencies.

This segment will handle investigations and backup for law enforcement, which underscores the government’s dedication to combating financial fraud within this rapidly evolving industry.

Nevertheless, the Financial Conduct Authority (FCA) has taken such a firm position that cryptocurrency companies are becoming increasingly irritated. Numerous entities have expressed dissatisfaction over prolonged waiting periods and insufficient responses during the registration phase.

Certain businesses are opting to expand internationally, choosing jurisdictions with more favorable legal systems for their operations, while still catering to UK customers. This situation, however, stirs debate about the competitive edge of the UK in the cryptocurrency sector, particularly for entities preferring less stringent regulations for their activities.

The Future Of Crypto In The UK

In the upcoming term under the new Labor administration, the fate of cryptocurrency regulations hangs in uncertainty; the current UK government has delayed or postponed plans regarding cryptocurrencies.

Despite the Financial Conduct Authority’s aim to facilitate company registrations, the high rate of failures suggests there is much work left to build trust and clarify the system.

The pressure is growing on authorities and businesses to find a workable compromise between adherence and innovation, as just 44 companies have successfully registered since the Financial Conduct Authority (FCA) began overseeing this sector.

Until the new regulations outlined in MiCA are implemented, it’s likely that the cryptocurrency sector within the UK will continue to face challenges.

Read More

- SOL PREDICTION. SOL cryptocurrency

- LUNC PREDICTION. LUNC cryptocurrency

- SHIB PREDICTION. SHIB cryptocurrency

- BTC PREDICTION. BTC cryptocurrency

- USD COP PREDICTION

- Red Dead Redemption: Undead Nightmare – Where To Find Sasquatch

- USD ZAR PREDICTION

- CAKE PREDICTION. CAKE cryptocurrency

- Top gainers and losers

- USD PHP PREDICTION

2024-09-07 01:12